Adopted Tax Rates for Real and Personal Property

NELSON COUNTY BOARD OF SUPERVISORS

APRIL 27, 2026 at 7:00 P.M.

PRESENT: Supervisors Jesse Rutherford, A. Cameron Lenahan, Jessical Ligon, Ernie Reed, and David Parr

ALL REFERENCED DOCUMENTS IN THE BOARD OF SUPERVISORS’ (BOS) PACKET can be found by going to https://www.nelsoncounty-va.gov/government/board-of-supervisors/, clicking on the calendar, April 27, 2026 and clicking on the 7:00 meeting announcement. It will be on left side of the page, 3rd item listed just above the agenda.!!!

I. The Meeting was CALLED TO ORDER.

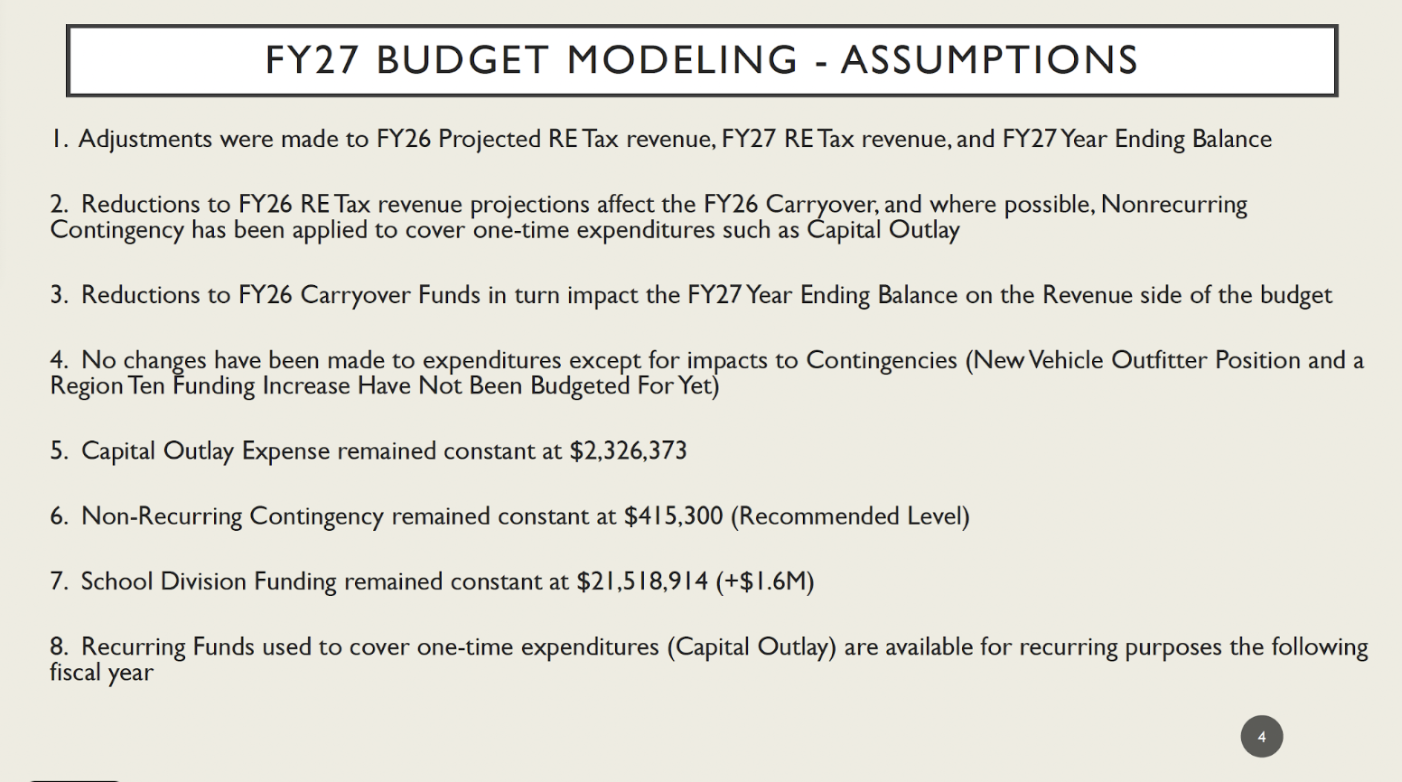

II. FY27 BUDGET CONSIDERATIONS:

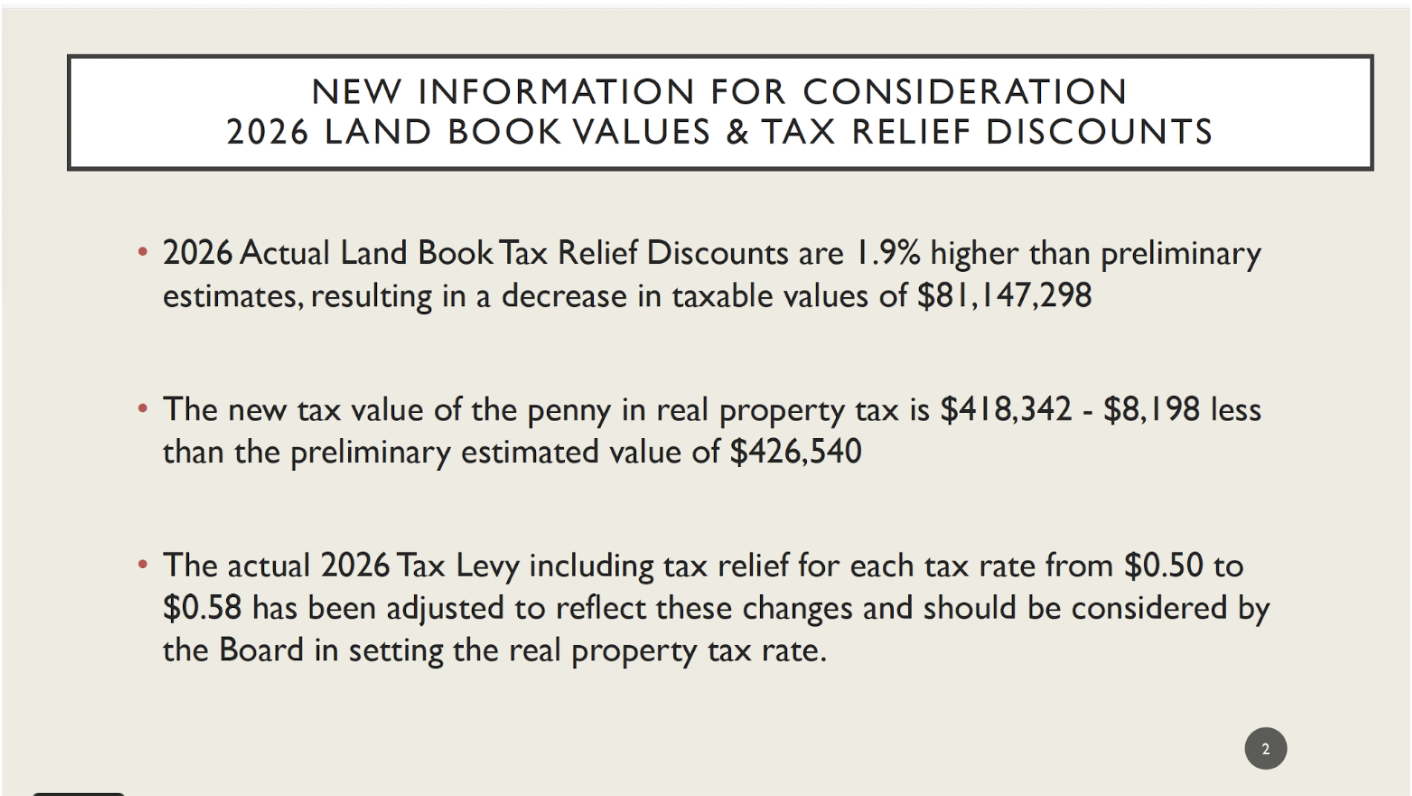

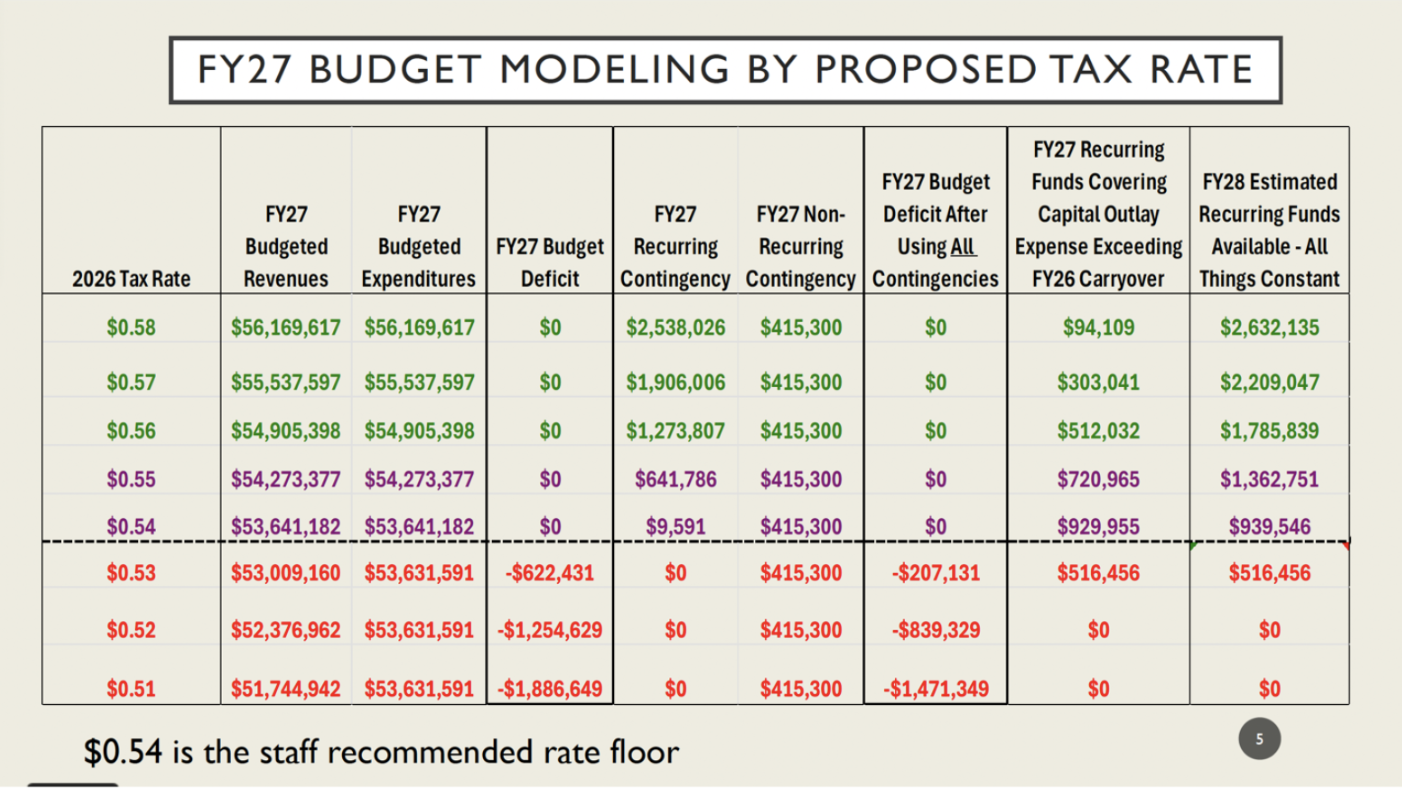

The original report submitted by Candace McGarry to the Board in the meeting packet appears below but was further modified by the information in the power point which followsthe report and the graphs. The 2026 Actual Land Book Tax Relief Discounts “are 1.9% higher than preliminary estimates, resulting in a decrease in taxable values of $81,147,298.” To generate the necessary projected revenues, the Board needed to increase the tax rate by .$01 over the previous projections.

“To: Board of Supervisors

From: Candy McGarry, County Administrator

RE: New Tax Rate Information – 2026 Actual Land Book Values Compared to 2026

Estimates Analysis

Attachment: 2026 Actual Land Book Values Compared to 2026 Estimates Analysis

Narrative Explanation:

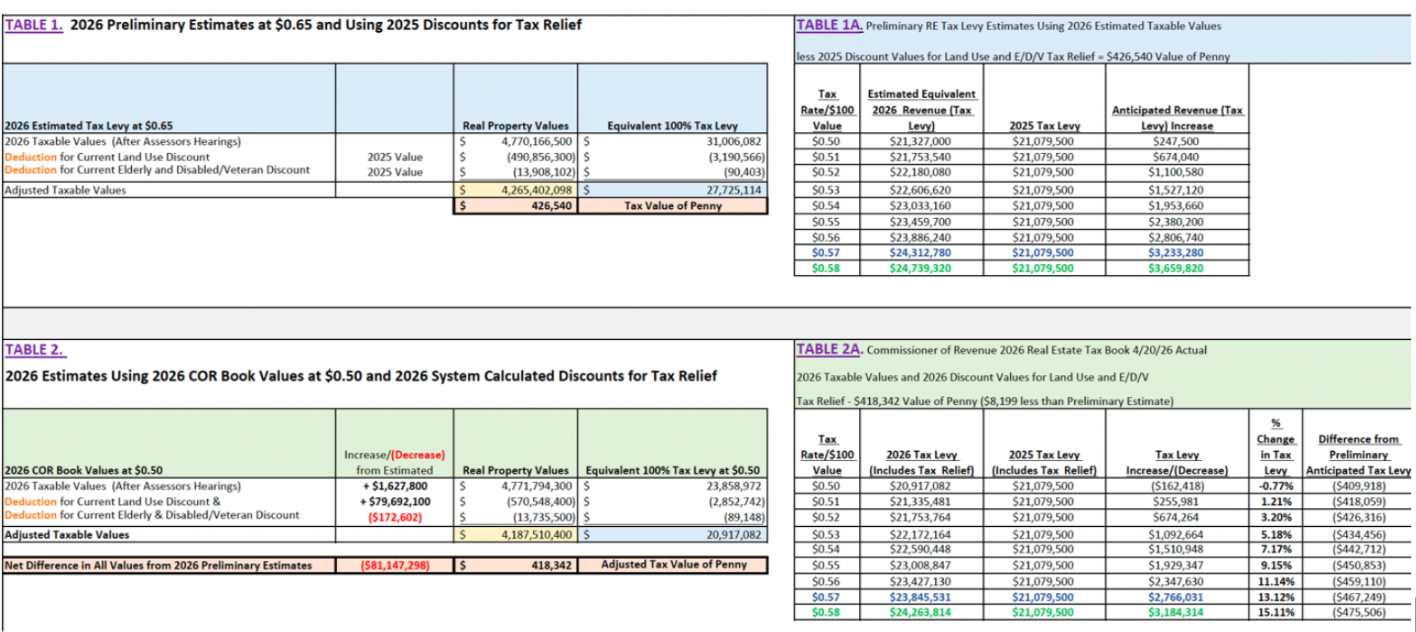

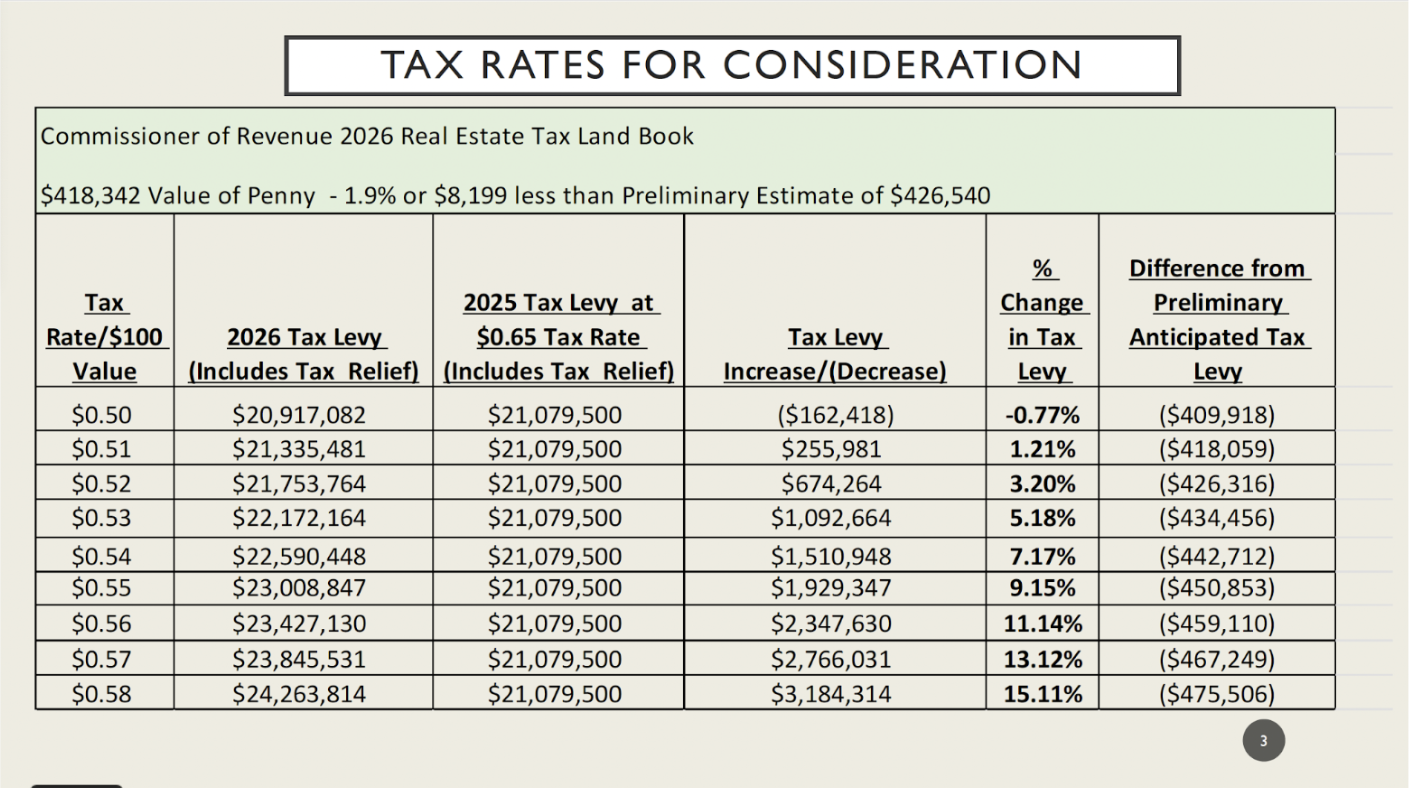

The actual system generated discounts for 2026 tax relief were $81,147,298 MORE than the 2025 discounts, which were used in preliminary estimates of the 2026 adjusted taxable values of $4,265,402,098 and associated value of the Penny in tax rate of $426,540 (See Tables 1 & 2). The actual system generated adjusted taxable values of $4,187,510,400 is $81,147,298 LESS than the estimated values and the associated value of the Penny in tax rate is $8,198 LESS than the estimated value of the Penny in tax rate at an actual amount of $418,342. (See Table 2) To date, the tax rates being discussed have been based on the estimated value of the Penny in tax rate of $426,540. With the actual value of the Penny in tax rate being $418,342, the associated anticipated revenues with each level of tax rate from $0.50 - $0.58 (maximum) should be considered in establishing the 2026 tax rate for real property and mobile/manufactured homes. (See Tables 1A & 2A)

It is important to note that a real property tax rate of $0.50 now generates LESS revenue than in 2025 and is not recommended for consideration.

Estimated VS. Actual Comparison:

Tax Relief Discounts Affecting Adjusted Taxable Values, Value of the Penny in Tax Rate, Estimates of Anticipated Tax levy, and Associated Increase in Revenue Generated at $0.50 - $0.58 intervals differ between Estimates and Actual:

I. Estimated – Calculations Used to Date

2026 Preliminary Estimates: Adjusted Taxable Values & Tax Value of Penny (TABLE 1.)

• 2025 property values associated with the deductions for Land Use, Elderly & Disabled, and Veteran tax relief were used in 2026 Preliminary Estimates

• 2026 Preliminary Estimates using these 2025 values and deductions resulted in Adjusted Taxable Values of $4,265,402,098 and a Tax Value of the Penny in Real Property Tax of $426,540

2026 Preliminary Estimates: Estimated Tax Levy and Increase in Generated Revenue

from 2025 (TABLE 1A.)

• The chart in TABLE 1A showing the estimated tax levy and associated increases in anticipated tax levy per Tax Rate of $0.50-$0.58 has been used in considering the establishment of the 2026 tax rate and in building the draft FY27 budget.

For Example:

o Advertised proposed Rate of $0.58 = $3,659,820 in anticipated new tax levy

o FY27 Draft budget is based on $0.57 = $3,233,280 in anticipated new tax levy

II. Actuals – System Generated Land Book Values

2026 Actuals: Adjusted Taxable Values & Tax Value of Penny (TABLE 2.)

• 2026 property values associated with the deductions for Land Use, Elderly & Disabled, and Veteran tax relief are higher than the 2025 property values for these discounts used in the 2026 Preliminary Estimates by $81,147,298. These are system generated when the Commissioner of Revenue processes the land book.

• 2026 Actual land book values and the system generated relief deductions, resulted in Adjusted Taxable Values of $4,187,510,400, a difference of $81,147,298 less than estimated. The new/actual Tax Value of the Penny in Real Property Tax is $418,342

2026 Actuals: Actual Tax Levy and Increase in Generated Revenue from 2025

(Decrease from Estimated) (TABLE 2A.)

• The chart in TABLE 2A, shows the actual tax levy and associated increases in anticipated tax levy per Tax Rate of $0.50-$0.58 that should be used now in considering the establishment of the 2026 tax rate and in finalizing the FY27 budget.

For Example, NEW actual tax levies are as follows:

o Advertised proposed rate of $0.58 = $3,184,314 in anticipated actual new tax levy - $475,506 LESS than the estimated amount of $3,659,820

o FY27 draft budget is based on $0.57 = 2,766,031 in anticipated actual new tax levy - $467,249 LESS than the estimated amount of $3,233,280

The corrected projected revenue data appears in the following power point:

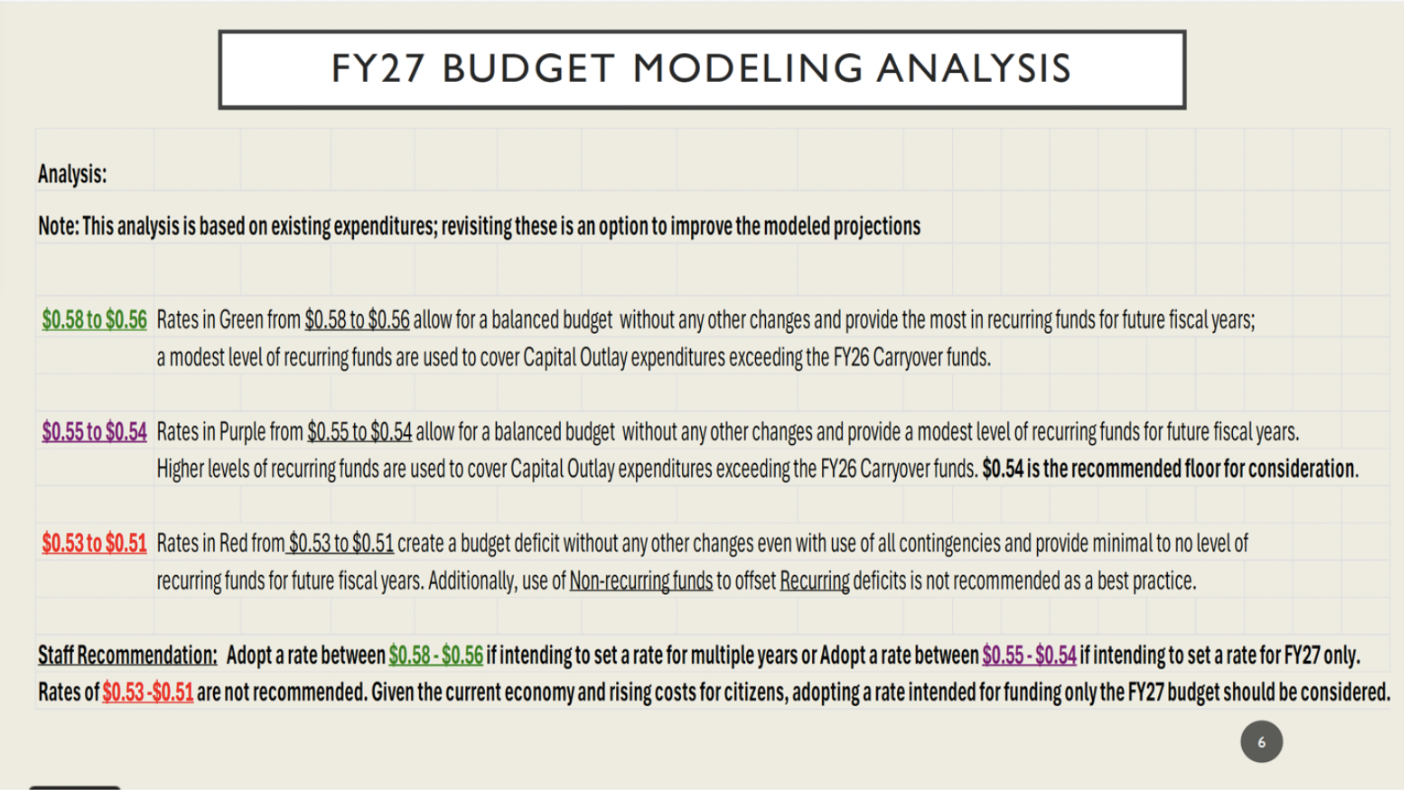

III. ESTABLISHMENT OF 2026 TAX RATES (R2026-35): In light of the revised revenue projections, the Board voted 4-1 to adopt the rates in Resolution 2026-35 set out here. Supervisor Lanahan was the dissenting vote.

“RESOLVED, by the Nelson County Board of Supervisors, pursuant to and in accordance with §58.1- 3001 of the Code of Virginia, 1950, that the tax rate of levy applicable to all property subject to local taxation, inclusive of public service corporation property, shall remain effective until otherwise reestablished by said Board of Supervisors and is levied per $100 of assessed value as follows:

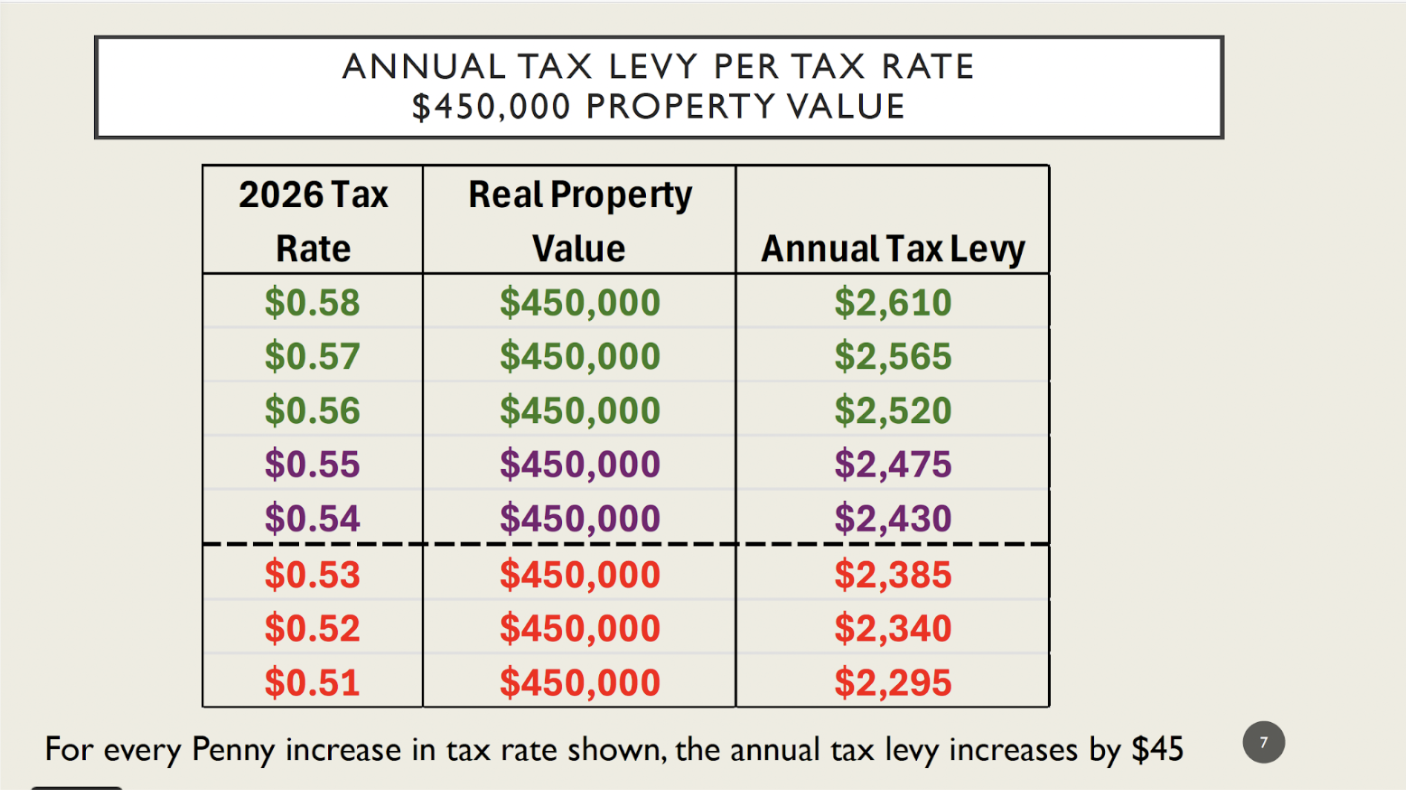

Real Property Tax $0.56

Tangible Personal Property $2.79

Machinery & Tools Tax $1.25

Manufactured Home (Mobile Home) Tax $0.56”

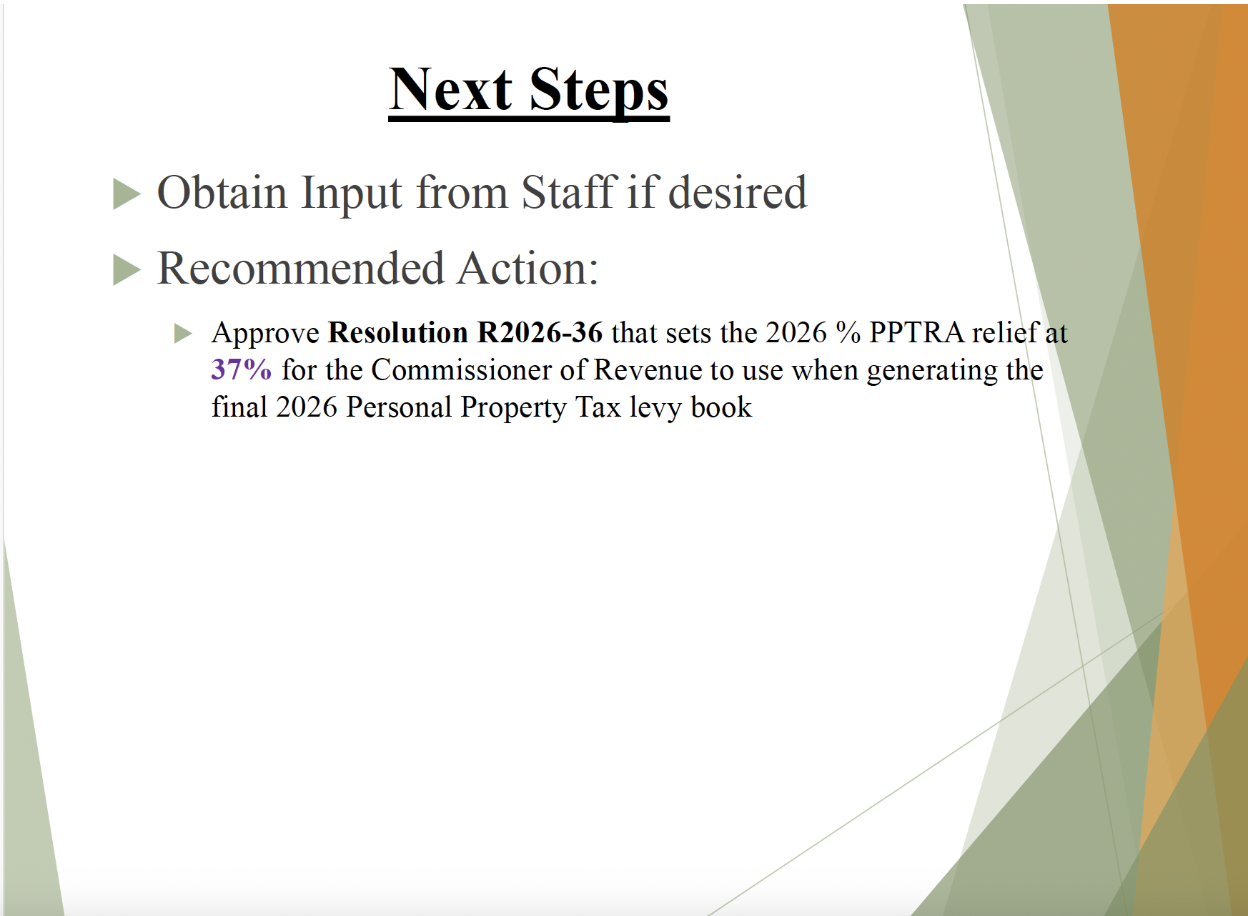

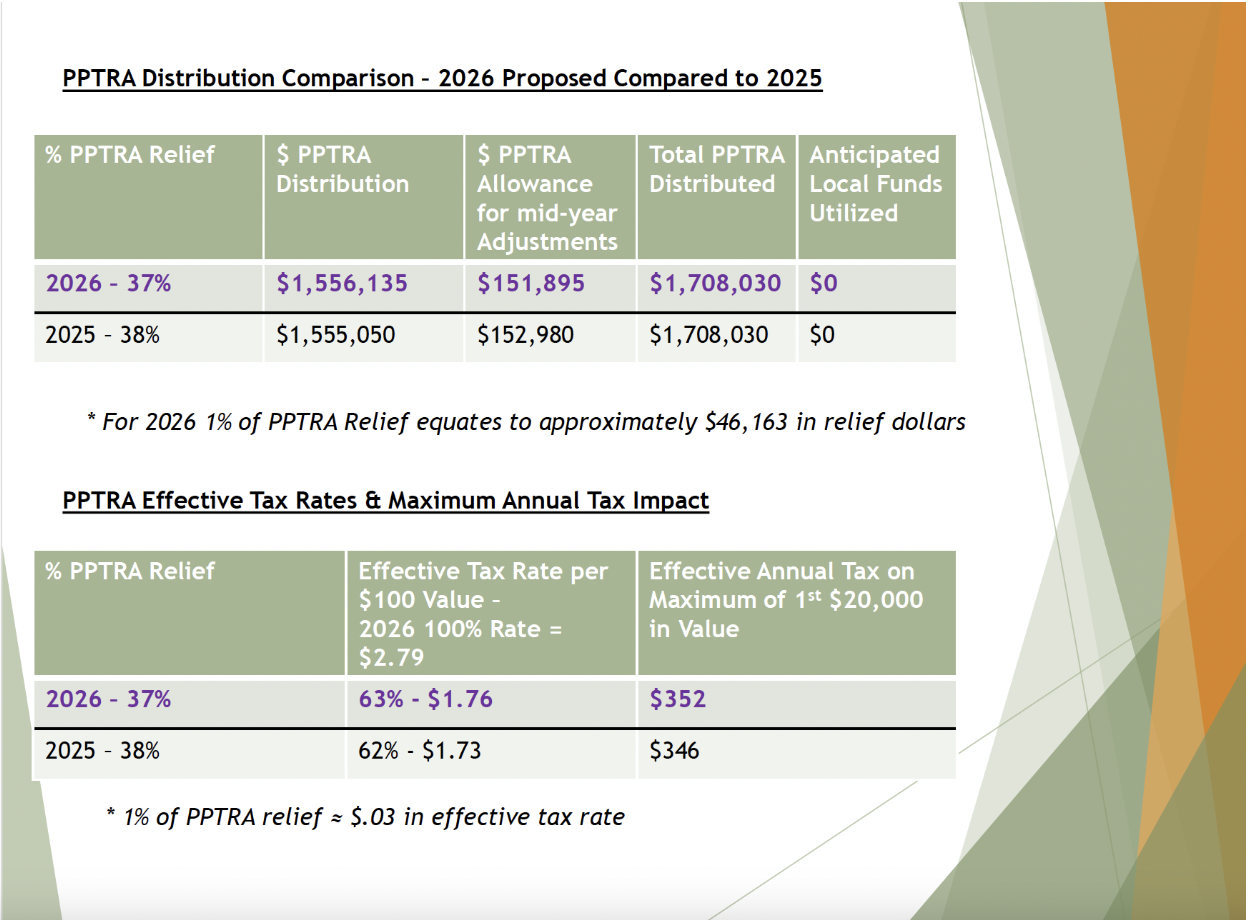

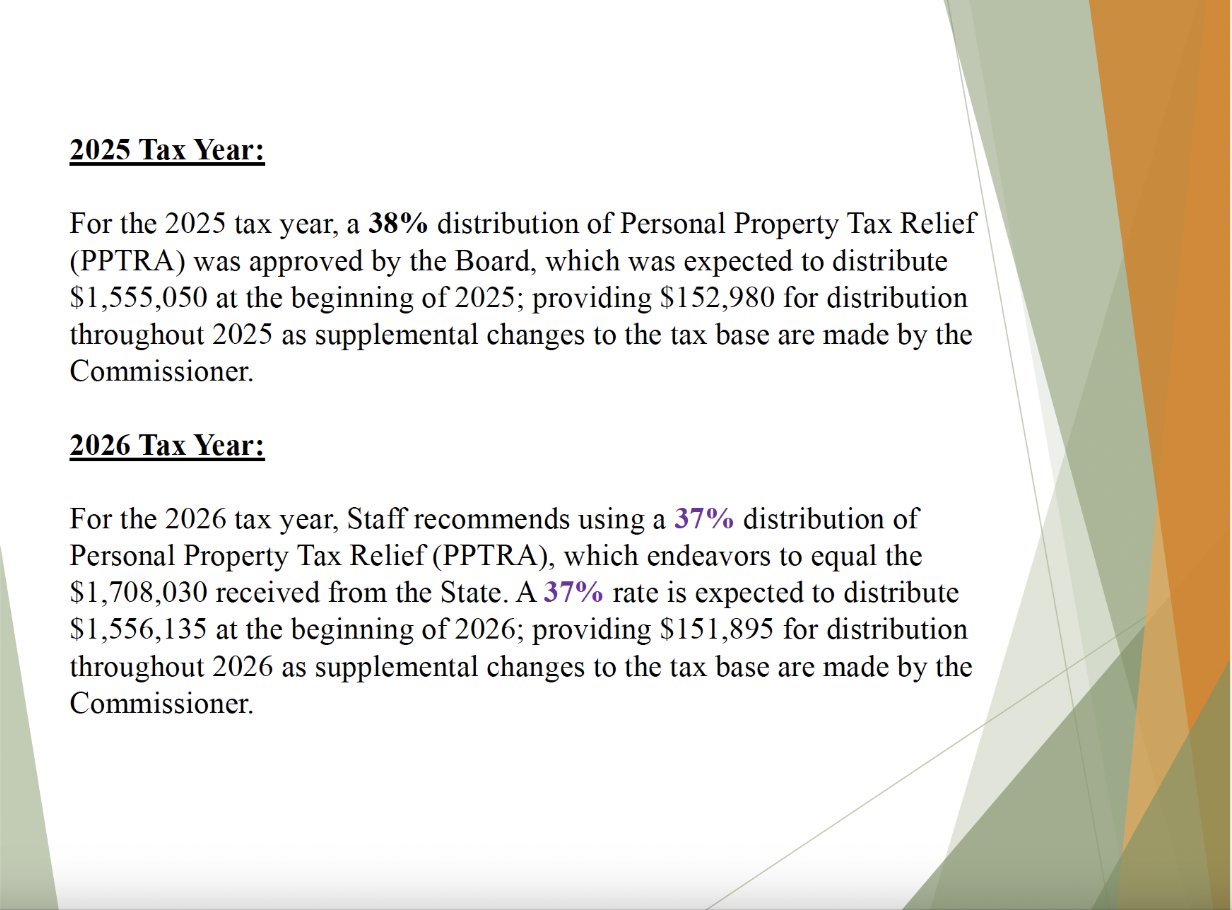

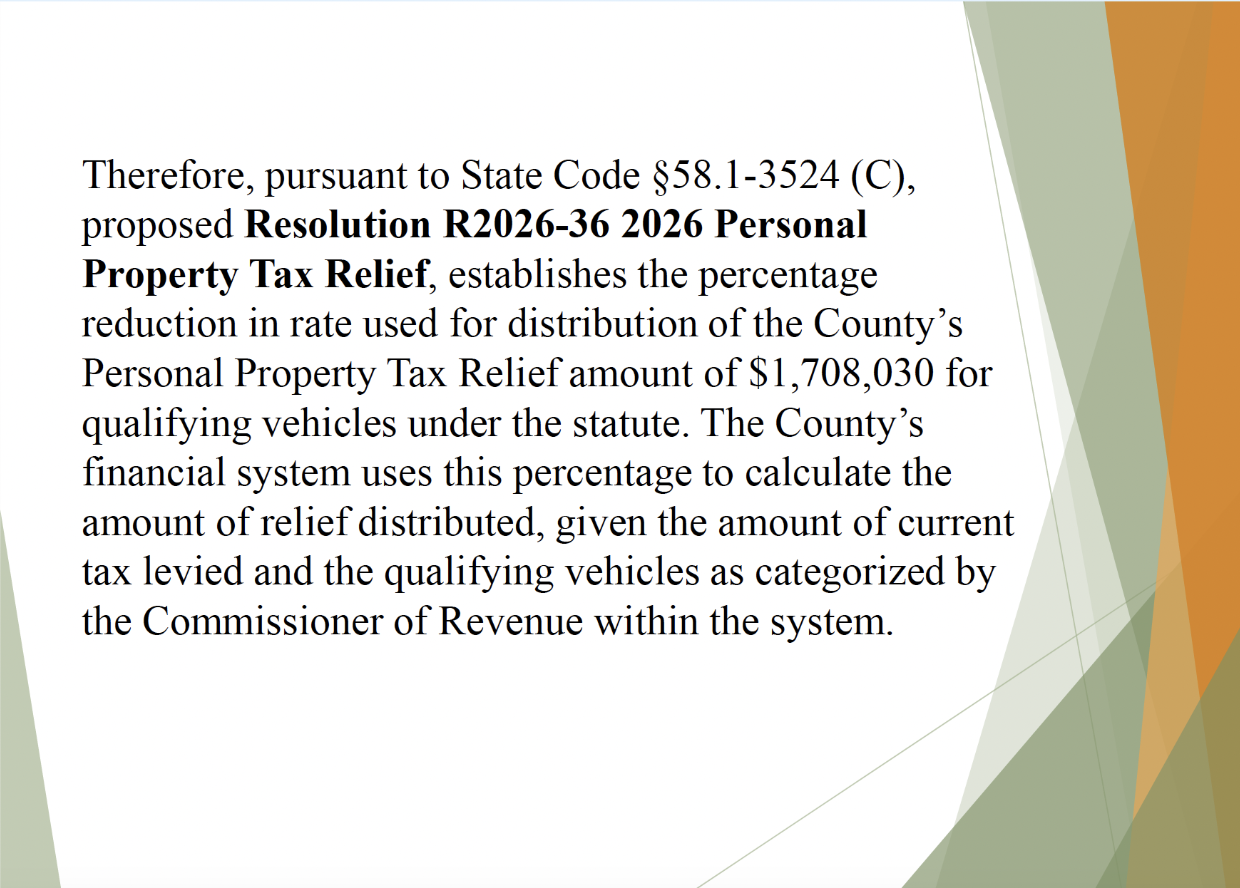

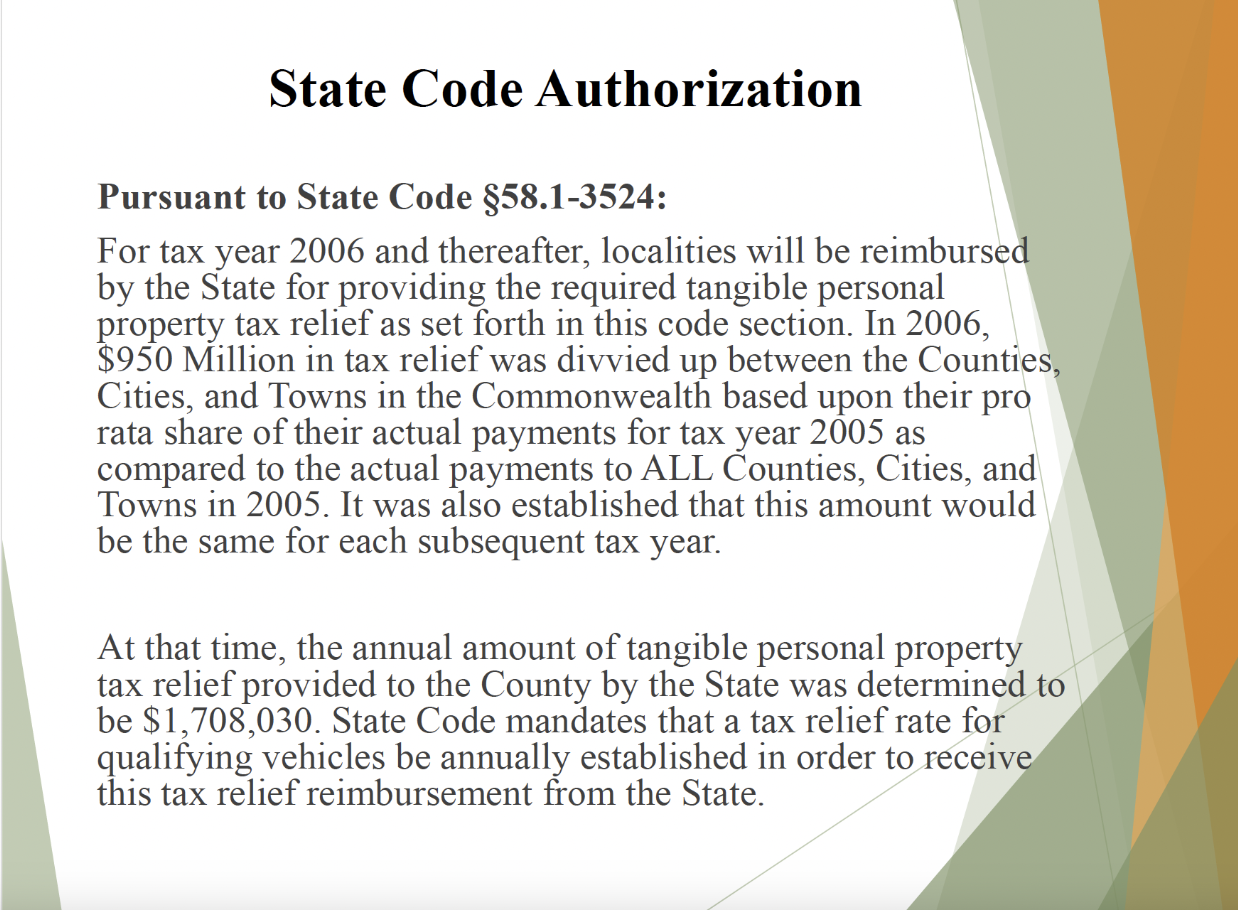

IV. ESTABLISHMENT OF 2026 PERSONAL PROPERTY TAX RELIEF (R2026-36): Candace McGarry reported to the Board the information contained in the power point below regarding the personal property tax relief.

The Board unanimously adopted the following:

“RESOLUTION R2026-36 2026 PERSONAL PROPERTY TAX RELIEF

“WHEREAS, the Personal Property Tax Relief Act of 1998, Va. Code § 58.1-3524 has been substantially modified by the enactment of Chapter 1 of the Acts of Assembly, 2004 Special Session I (Senate Bill 5005), and the provisions of Item 503 of Chapter 951 of the 2005 Acts of Assembly; and

WHEREAS, the Nelson County Board of Supervisors has adopted an Ordinance for Implementation of the Personal Property Tax Relief Act, Chapter 11, Article X, of the County Code of Nelson County, which specifies that the rate for allocation of relief among taxpayers be established annually by resolution as part of the adopted budget for the County.

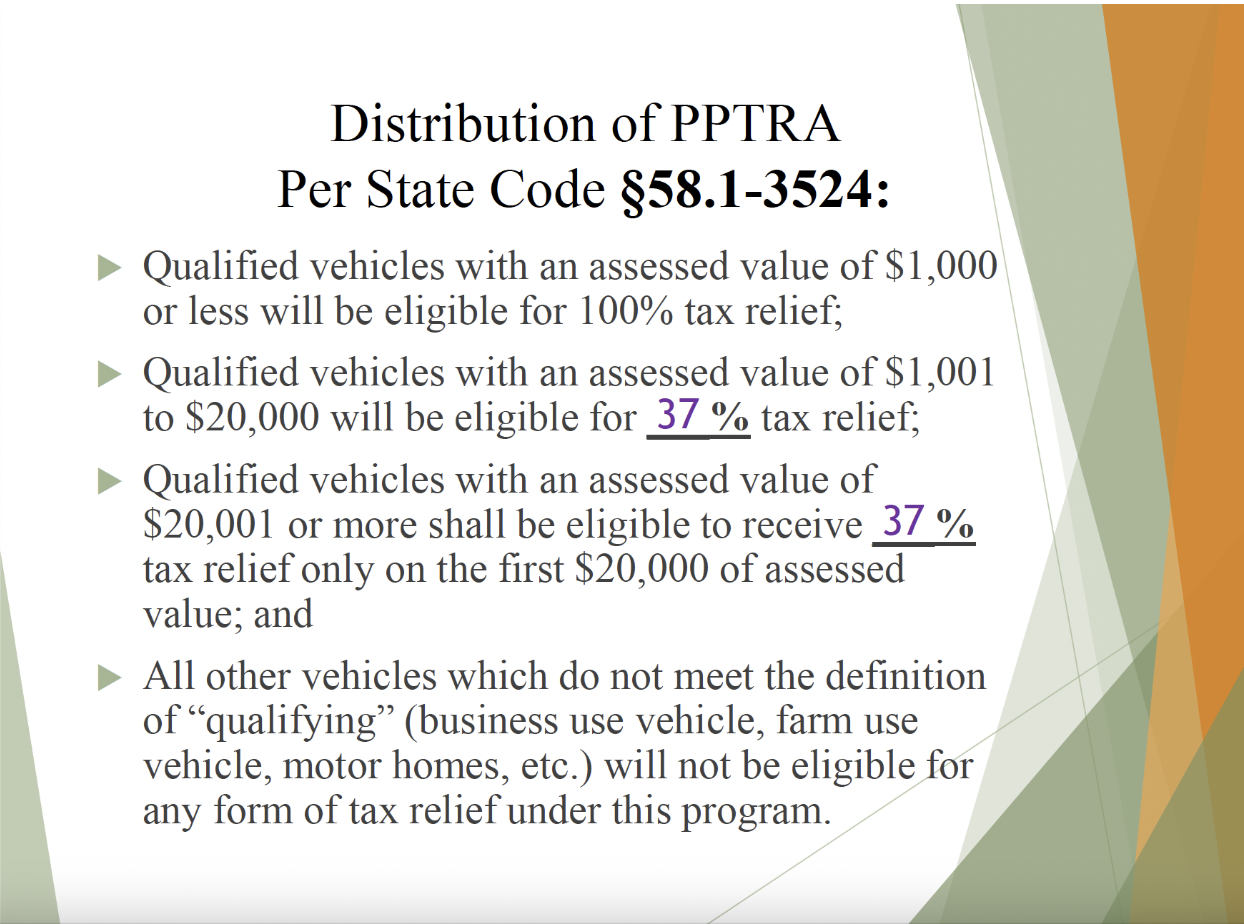

NOW THEREFORE BE IT RESOLVED that the Nelson County Board of Supervisors does hereby authorize tax year 2026 personal property tax relief rates for qualifying vehicles as follows:

• Qualified vehicles with an assessed value of $1,000 or less will be eligible for 100% tax relief;

• Qualified vehicles with an assessed value of $1,001 to $20,000 will be eligible for 37% tax relief;

• Qualified vehicles with an assessed value of $20,001 or more shall be eligible to receive 37% tax relief only on the first $20,000 of assessed value; and

• All other vehicles which do not meet the definition of “qualifying” (business use vehicle, farm use vehicle, motor homes, etc.) will not be eligible for any form of tax relief under this program.

BE IT FINALLY RESOLVED that the personal property tax relief rates for qualifying vehicles hereby established shall be effective January 1, 2026 through December 31, 2026.”

V. OTHER BUSINESS (AS PRESENTED):

A. Request for Reconsideration of Special Use Permit #250263 – Morse Lane Campground: The following request for reconsideration was received by Supervisor Ligon:

“Request for Reconsideration of Special Use Permit #250263 – Morse Lane

Campground

Dear Nelson County Board of Supervisors,

I’m writing regarding the denial of Special Use Permit 250263 for the glamping-style campground on Morris Lane. The project, located on tax map parcels 7-6-5-4, 35.9 acres owned by Tim and Lori Beth Masters, and 76-5-5, 77.5 acres owned by Nelson Morris Lane Land Trust, received unanimous approval from the Planning Commission on March 25th and fully complies with every objective requirement in the county zoning ordinance, environmental standards, and tourism development goals. The Board’s 3-2 denial was based on unsubstantiated neighbor complaints and personal comments rather than the established criteria. This decision was arbitrary and capricious, and it failed to uphold the county’s own standards and economic objectives. Under Section 2-52(f) of your adopted Rules of Procedure, after a vote has been taken on a matter before the board, any member may move for its reconsideration, provided such motion is made at the same meeting or an adjournment thereof at which the matter was originally acted upon. I respectfully request that the Board schedule reconsideration and a revote at the earliest possible meeting. I remain committed to responsibly developing my property in alignment with Nelson County’s tourism vision. I would appreciate a response within two weeks confirming whether the Board intends to reconsider this matter.

Sincerely,

Tim Masters”

Supervisor Parr moved to grant a reconsideration. The vote was 4-1 with Supervisor Reed dissenting. Supervisor Parr moved to send/refer the matter back to the planning commission which was unanimously approved. Supervisor Parr expressed that his reason for both motions was protect the Board from legal action by the applicant because the reasons for the Board’s actions had not been fully articulated and this motion does not mean he had changed his mind from his original vote.

Supervisor Parr told the Board that new information had been received about the proposed relocation of the School Board offices which would need the Board’s attention in the near future.

VI. The meeting was unanimously ADJOURNED.